.svg)

.svg)

9 Perspectives on Mortgage Points and Fees Every Homebuyer Should Understand

TL;DR

Mortgage points and lender fees have quietly climbed to their highest level in two decades, subtly increasing the true cost of homeownership. This list breaks down why these costs matter, how buyers can weigh the gamble of paying points, and what each fee really means in the context of shifting market rates and long-term value.

Understanding the Impact of Mortgage Points and Fees

A realistic home office desk arranged with mortgage paperwork, calculator, and closing cost disclosures, illustrating the decision-making process.

Mortgage fees and points are reaching historic highs, with most buyers now encountering lender charges just under 1 percent of their loan. For anyone navigating the home purchase in this climate, understanding exactly what you are paying for is critical. These costs, often folded quietly into closing costs, can affect both your immediate out-of-pocket investment and your long-term household expenses. Buyers today are faced with the decision of whether to pay mortgage points to lower their interest rate or to keep more cash on hand by accepting a higher rate. Each choice involves a calculated risk that hinges on future market conditions, personal finances, and the fine print of the purchase contract. This guide offers clear perspectives on how these fees work, ways to compare their value, and several concrete scenarios to help you make smarter decisions when calculating the true price of homeownership.

-

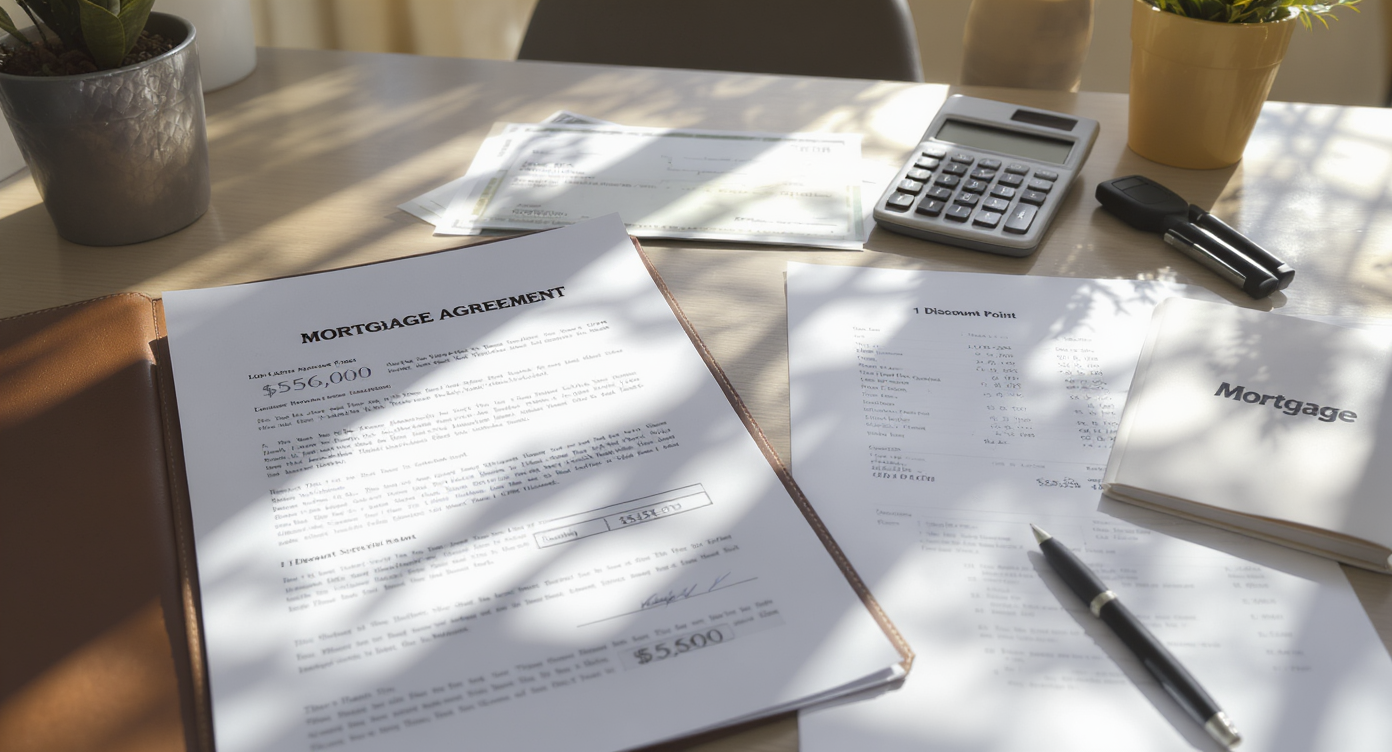

1. Mortgage Points Explained: What Are You Really Paying?

A realistic home office scene showing mortgage documents, a calculator, and a $5,600 discount point breakdown for a $560,000 loan.

Mortgage points, also known as discount points, represent upfront fees paid to lenders in exchange for a lower interest rate on your mortgage. Typically, one point equals one percent of the loan amount. For example, on a $560,000 loan, one point equates to $5,600. This fee is not mandatory, but paying it resets your interest rate, creating a bet on how long you will keep the loan. Financial professionals often stress that while points can reduce your monthly payment, they may not always make sense depending on how long you plan to own the home.

-

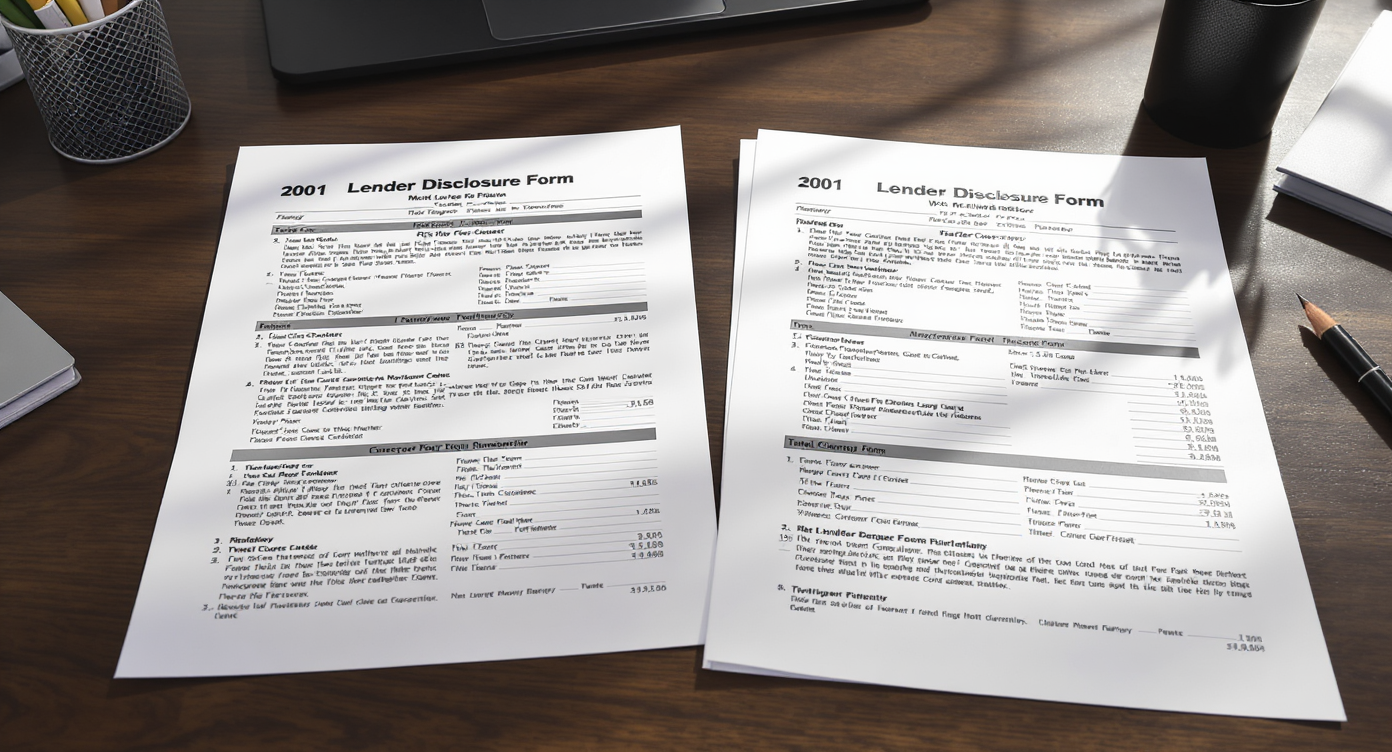

2. Current Trends: Why Fees Are Hitting Two-Decade Highs

Side-by-side lender disclosure forms from 2001 and today, with visible fee differences, highlight why mortgage fees are reaching two-decade highs.

Recently, average mortgage fees have approached one percent, echoing figures not seen since 2001. While interest rates are a visible part of home financing, the cost of lender fees like underwriting, processing, and discount points has crept steadily upward. This means today's buyers are frequently paying more upfront, quietly increasing the true closing costs associated with purchasing a home. As detailed in our breakdown of closing costs, most buyers now need to be more careful when reviewing lender disclosures and calculating their bottom line.

-

3. 'Closing Costs'—Lumping or Hiding the Real Numbers

The term 'closing costs' often hides the breakout of actual fees paid to secure a loan. While resources commonly estimate closing costs as two to five percent of the purchase price, the reality is more nuanced. Lender fees, title insurance, appraisals, and taxes may all be included but are rarely detailed upfront in a way that emphasizes their impact. As we explored in our article about avoiding first-time buyer mistakes, not understanding closing cost components can lead to unpleasant surprises at the final signing—especially when lender fees quietly make up a significant slice.

-

4. The Break-Even Dilemma: How to Calculate True Savings

Determining whether to pay mortgage points hinges on calculating your break-even period. This is the point where your upfront costs are offset by your monthly savings from a reduced rate. The formula involves dividing the cost of the points by the monthly payment savings and then dividing that result by 12. For instance, if you pay $5,000 in points and save $76 per month, your break-even is roughly 66 months—over five years. Careful value comparison between upfront spending and monthly savings helps ensure buyers do not overcommit to points when future rate shifts or refinancing could erase those savings.

-

5. Cost-Aware Prompts: Should You Buy Points or Keep Cash?

A workspace visually comparing options: mortgage calculator app, cash reserve, and down payment folder for mortgage decision analysis.

Choosing whether to pay points, keep cash, or even use funds for a larger down payment is a strategic decision. Designers of mortgage calculators and financial planners recommend modeling each scenario: pay points, increase your down payment, or simply retain flexibility with cash reserves. For example, applying $5,000 toward a larger down payment instead of buying mortgage points may result in both a lower monthly payment and greater financial flexibility should rates drop and refinancing options arise. In uncertain markets, such cost-aware prompts can help buyers remain agile.

-

6. Rate Buydowns and Unexpected Market Shifts

If you opt to pay points and rates later fall, your investment in buying down the rate can become a sunk cost—especially if a refinance becomes attractive before reaching your break-even. Professionals working in dynamic markets report many buyers who paid points during rate spikes were frustrated to see refinancing opportunities appear just a year or two later. As we discussed in our overview on first-home financing, market cycles and rate volatility can significantly impact whether buying points was worthwhile in retrospect.

-

7. The Difference Between Purchase and Refinance Fees

Refinancing typically involves fewer ancillary costs than an initial home purchase. For example, transfer taxes and certain title fees are often lower or absent in a refinance. As a result, the costs associated with refinancing tend to be more transparent and limited. Buyers should consider that paying substantial mortgage points at purchase can, in some cases, equal several rounds of refinance closing costs, as highlighted in recent consumer analyses.

-

8. State and Local Variations in Lender Fee Structures

Folders labeled by state display varied mortgage fee documents, illustrating how lender charges differ significantly across U.S. regions.

Lender fees and associated costs vary significantly between regions. For example, some states impose additional taxes on mortgage transactions or have higher title insurance premiums, impacting total lender fees. Homebuyers in places like Florida encounter unique charges, such as documentary stamp and intangible taxes on certain transactions. When using listing visuals or comparing options across regions, always ensure you factor in these state-specific considerations for an accurate value comparison. Resourceful buyers often review local norms alongside national averages to identify savings opportunities.

-

9. Negotiating Power: Buyer Credits, Seller Concessions, and Fee Transparency

A realistic home office setup with a laptop, organized folders, and documents for modeling mortgage points, buyer credits, and seller concessions.

The evolving real estate landscape now offers more room for negotiation on lender fees. Recent regulatory shifts have made it possible for buyers and sellers to share costs creatively, sometimes using seller credits or negotiated agent fees to offset expensive points. If you are uncertain about your options, technology platforms like REimagineHome.ai allow you to model scenarios, test out how different fee structures and credits will impact your bottom line, and bring clarity to complex transactions. As commission structures change, buyers gain new tools for informed negotiation. For further reading on shifting agent fees and deal structures, see our insights into commission resets and buyer agent fees in today's market.

Frequently Asked Questions About Mortgage Fees and Points

Mortgage points are prepaid amounts to reduce your interest rate, while lender fees include processing, underwriting, and other costs to originate your mortgage.

How do I know if paying points is worth it?

Use a break-even formula (cost of points divided by monthly savings divided by 12) to estimate how many months it will take for your upfront investment to pay off. If you plan to keep the mortgage longer than this period, it may be sensible. Tools at REimagineHome.ai can help with estimates.

Are all closing costs negotiable?

Not all closing costs are negotiable, but lender fees and certain third-party expenses often are. Negotiating credits or concessions can help reduce your net expenses.

Does every state have different lender fee norms?

Yes, local taxes, title insurance rates, and standard practices differ significantly and can impact the total lender fees and closing costs you will face.

Where can I learn more about budgeting for home purchase and closing costs?

Our detailed guide, How to Buy Your First Home: Budgeting, Mortgage Tips, and Closing Cost Breakdown, offers step-by-step strategies.

Key Takeaways for Smarter Mortgage Fee Decisions

Understanding the intricacies of mortgage points and lender fees is more essential than ever, as these costs quietly raise the bar for new homebuyers. Smart planning requires not only a keen eye for closing cost line items but also a willingness to model multiple scenarios and test assumptions. Platforms like REimagineHome.ai, along with informed guidance from professionals, can give buyers the insight they need to make decisions that remain valuable regardless of market volatility or rule changes.

.png)